INSIGHTS: The income play built for uncertain markets

20 April 2026

By Mark Power, Head of Income Credit at Qualitas

Rising interest rates. Persistent inflation. Growing uncertainty in global credit markets. For many investors, these signals point to increased risk.

But for the Qualitas Real Estate Income Fund (ASX:QRI), today’s market conditions are a source of opportunity. In fact, the same forces creating volatility are helping to reinforce the fund’s focus on delivering consistent income at attractive risk-adjusted returns1 and seeking to protect capital.

Why higher interest rates can work in QRI’s favour

A common assumption I hear from investors today is that when interest rates rise, real estate suffers.

That may hold true for equity investors, as property values come under pressure. But QRI sits in the credit layer of the capital stack, where the dynamics are fundamentally different. Due to the fund’s set up, QRI investors have a significant capital buffer protecting their investment (more on that later).

So how can rising rates benefit QRI investors? Firstly, the fund’s portfolio is 100% floating rates, with loans repriced around every 30 days. That means as interest rates increase, this uplift flows directly through to income distributions to our investors.

Secondly, higher rates and macroeconomic volatility tend to take liquidity out of the market. Financiers backed by retail and wholesale capital are forced to pull back due to potential redemption pressures, creating a market dislocation and opening up opportunities for financiers like Qualitas who are backed by institutional capital. So rather than making our job harder, higher rates actually improve the quality of opportunities we see. For example, during a period of thirteen interest rate hikes between 2022 and 2024, the total loans we deployed grew by around 30% per year.

Thirdly, there is a structural tailwind at play within residential property. As cost-of -living pressures rise and borrowing capacity tightens, demand shifts towards more affordable housing – particularly apartments. The average Aussie household is already taking 22% longer to save for a house deposit compared to 20 years ago2 – and that’s before these latest headwinds set in. QRI is heavily positioned in the residential apartment sector as we have strong conviction in that part of the market.

Crucially, these positive outcomes only become possible if a portfolio can absorb rate pressure. We’ve built QRI’s loan book with this environment in mind, invasively assessing each and every borrower for their ability to absorb higher rates and withstand downside scenarios. Every investment we make is stress tested at the outset – meaning the current environment is something the portfolio has been deliberately designed to handle.

Built with the aim of protecting capital – and delivering consistent income

In uncertain markets, resilience matters more than ever.

QRI’s track record reflects our clear focus on capital preservation and reliable income. Since its launch in 2018, the fund has recorded no impairments and currently has no workouts3. Plus, it’s consistently delivered monthly income to investors – with 7.14% distributed in the past twelve months and 7.40% p.a. since launch.

This consistency is underpinned by a deliberately defensive portfolio:

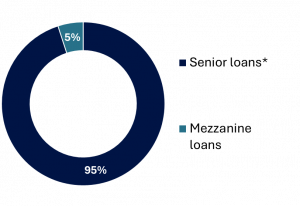

- 95% of investments are in senior loans

- the average loan-to-value ratio (LTV) is around 65%

- the fund contains 58 loans, providing good diversification while still allowing thorough oversight

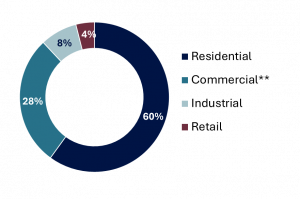

- Around 70% of loans are in the residential and living sectors.

QRI LOAN RANKING4 QRI PROPERTY SECTOR EXPOSURE3

*Senior loans (excludes Trust loan receivable and cash) include first ranking loans (84%), and Senior subordinated loans (11%). Senior subordinated loans are subordinated in repayment priority to the senior financier under a common first ranking debt facility but rank ahead of any mezzanine facility.

**12.1% exposure in Accommodation Hotels grouped under Commercial.

This structure provides a meaningful buffer against market volatility. At a 65% LTV, the underlying property values would need to decline by around 35% on the weighted average basis before investor capital is materially at risk – and even more if the fund is trading below its net asset value.

Underpinning this is our highly rigorous due diligence framework. When we underwrite loans, we don’t assume benign conditions, we stress test everything: higher rates, slower sales, cost pressures and more. These are all scenarios we sensitise for both before we invest and right throughout the lifecycle of a loan.

So, when I look at what’s playing out today, it’s very much within the range of outcomes we’ve already planned for. The result is a portfolio that remains healthy, even as conditions become more challenging.

Tighter liquidity can provide opportunities for disciplined lenders

There’s been a lot of commentary recently around liquidity in private credit markets, particularly offshore.

However, much of this pressure is being driven by factors that don’t affect Qualitas – including exposure to sectors such as US software lending.

Locally, there is some noise around potential redemption pressures across parts of the market. But for QRI, this dynamic may actually prove beneficial.

With a predominantly institutional investor base and therefore minimal exposure to redemption risk, Qualitas has a stable pool of capital. This allows us to continue deploying capital even as others are forced to step back.

What makes QRI different?

Not all private credit strategies are positioned to benefit from today’s conditions. As liquidity tightens, success is increasingly driven by access, discipline and portfolio strength.

Qualitas possesses several structural advantages in this environment.

- A predominantly institutional capital base provides stability, allowing the QRI fund to deploy capital consistently rather than react to redemption pressures.

- Long-standing borrower relationships and deep origination networks enable access to high-quality opportunities, even as competitors pull back.

- A disciplined focus on senior lending, combined with rigorous underwriting and active portfolio management, enables the fund to prioritise capital preservation while selectively capturing improved risk-adjusted returns.

The two primary risks in real estate lending are a loss of loan principal and a loss of loan income. The first arises when a borrower cannot repay the loan and the security property’s value is insufficient to cover the outstanding amount. The second occurs when cash flow from the property or other borrower sources cannot meet the loan interest and fees owed to the lenders5.

We’ve designed QRI to be resilient enough to not only withstand, but benefit from periods of uncertainty. The conditions we’re seeing today are exactly the sort of scenarios we built this portfolio for.

>> Access smart investments made simple at qualitas.com.au/qri.

[1] The payment of monthly cash income is an objective of the Trust only and neither the Manager or the Responsible Entity provide any representation or warranty (whether express or implied) in relation to the payment of any monthly cash income. Returns are not guaranteed. The premium achieved is commensurate to the investment risk undertaken. Past performance is not a reliable indicator of future performance.

[2] PropTrack, October 2024

[3] As at 28 February 2026. Past performance is not a reliable indicator of future performance.

[4] The portfolio statistics are determined on a look-through basis having regard to the loans in the underlying Qualitas Funds as indicated. The classifications of these diversification parameters are determined by the Manager. Figures stated are subject to rounding.

[5] QRI PDS is available on QRI website https://www.qualitas.com.au/listed-investments/qri-overview

Disclaimer

This communication has been issued by The Trust Company (RE Services) Limited (ACN 003 278 831) (AFSL 235150) as responsible entity of The Qualitas Real Estate Income Fund (ARSN 627 917 971) (“Trust” or “Fund”) and has been prepared by QRI Manager Pty Ltd (ACN 625 857 070) (AFS Representative 1266996 as authorised representative of Qualitas Securities Pty Ltd (ACN 136 451 128) (AFSL 34224)). This communication contains general information only and does not take into account your investment objectives, financial situation or needs. It does not constitute financial, tax or legal advice, nor is it an offer, invitation or recommendation to subscribe or purchase a unit in QRI or any other financial product. Before making an investment decision, you should consider whether the Trust is appropriate given your objectives, financial situation or needs. If you require advice that takes into account your personal circumstances, you should consult a licensed or authorised financial adviser. While every effort has been made to ensure the information in this communication is accurate; its accuracy, reliability or completeness is not guaranteed and none of The Trust Company (RE Services) Limited (ACN 003 278 831), QRI Manager Pty Ltd (ACN 625 857 070), Qualitas Securities Pty Ltd (ACN 136 451 128) or any of their related entities or their respective directors or officers are liable to you in respect of this communication. Past performance is not a reliable indicator of future performance. The PDS and a Target Market Determination for units in the Trust can be obtained by visiting the Trust website www.qualitas.com.au/qri. The Trust Company (RE Services) Limited as responsible entity of the Fund is the issuer of units in the Trust. A person should consider the PDS in deciding whether to acquire, or continue to hold units in the trust.